The Equity build – Is it the right move?

Property investment has costs and risks. But is it still worth it long term, especially in an environment where equity gains do not feel certain?

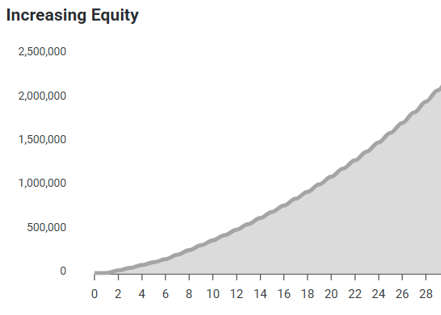

In terms of long-term gain, the benefits of using leverage — or what I call “negative money” — to buy a real-world asset is still a winner. We all know how amazing the numbers look, even when you take away inflation and compare property to a good-performing managed fund.

Based on historical returns in property (not always an indicator of the future), you could expect to see a $700k–$800k gain on an investment, using an approximate 3.9% return (taking out 2.2% inflation), after 15 years.

The costs of holding, if invested into a managed fund, would not quite get there — approximately $400k–$500k (after inflation) on a fund returning 8.10%. However, the managed fund would be less hassle (no interest rate risk or management) and could be partially liquidated at any time.

Impact on lifestyle – an honest look at costs

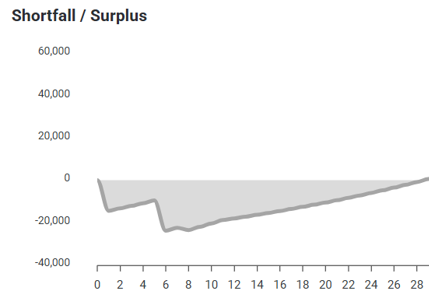

Buying an investment property for $750,000 with a rent of $650 per week could mean costs of more than $20,000 per year. This burden is a lot lighter during interest-only periods and starts to drop steadily after many years due to rent appreciation. Of course, you could argue that the property pretty much pays for itself, if you ignore maintenance and principal loan repayments.

However, it is important to understand the true costs and mitigate for them, as it is the ability to hold the property long term that really determines the amazing value added to your wealth.

Making your position stronger

Here’s the grammar-corrected version with content unchanged:

The costs of holding an investment property can be patchy — for example, maintenance bills do not always come up. To build some resilience into your own cashflow, you could build a buffer inside a revolving credit or get an additional facility at the onset. It is also important to have some understanding of your tax position. Very often our clients prefer to get an interest-only term on their investment home loans. Yes, this does cost you more in the long run; however, this cost can be nullified by redirecting those potential lost repayments into any debt against your main home.

To assist in building up a safety margin in terms of backup funds, it may be prudent to stretch the home loan term on your main home. This will increase the interest costs if the reduced cashflow gets diverted to spending instead of reducing revolving credit balances.

As always, talk to a good financial adviser like ourselves before embarking on growing your wealth with property.