How much impact does the mix of asset classes have on the fund?

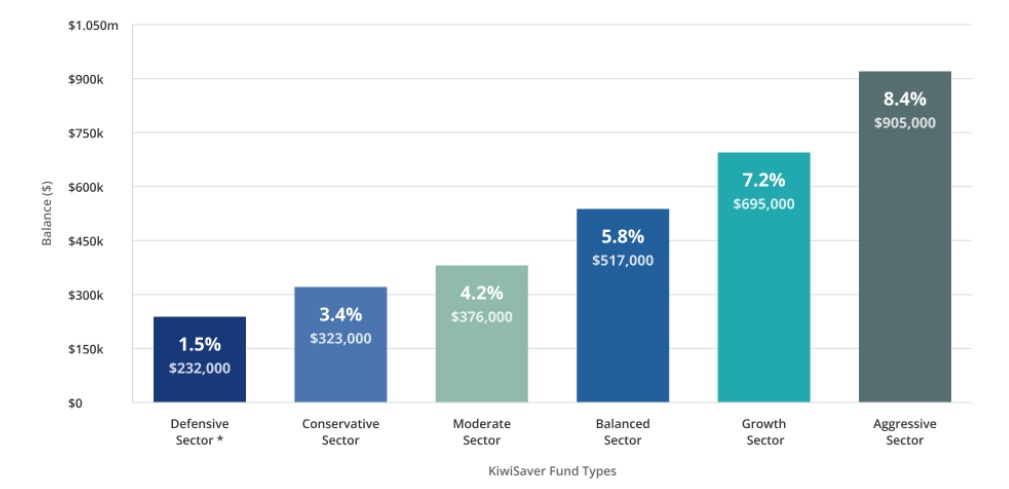

The mix of asset classes in a fund (for example, shares, property, fixed interest and cash) can have a major impact on long-term returns. In general, funds with a higher allocation to shares have tended to deliver higher long-term growth — but with a bumpier ride along the way.

To put the potential difference into perspective, we’ve seen modelling where the gap between the lowest-risk (least volatile) fund and the highest-risk (most volatile) fund was more than $500,000 over 30 years for someone starting on a $75,000 salary. That’s the kind of difference that can materially change retirement outcomes, especially when you start young and give compounding time to work.

That said, higher returns don’t come “for free”. More growth exposure usually means larger ups and downs in account balance. Those swings matter more when your timeframe is shorter — for example:

- If you’re nearing retirement, because there’s less time to recover from market drops.

- If you’re planning to use KiwiSaver for a first-home deposit, because you may need the money at a specific point in time.

The key is matching your fund’s risk level to your time horizon and tolerance for volatility.

Forecasting over the long term is challenging. Past performance is not a reliable indicator of future results, and this article is general information — not personalised financial advice.

Do fund providers have much of an impact on what I get in retirement?

Yes — providers can make a difference. Performance varies, and it’s not always obvious over short timeframes. Some asset classes and investment styles can look “out of favour” for years before they shine again, so judging a provider purely on recent performance can be misleading.

Fees also matter, but here’s the important nuance: the cheapest fund isn’t always the best outcome after fees. What ultimately counts is the net return after fees (and how consistently that provider delivers over time).

Why it can be worth reviewing your KiwiSaver

It can make sense to review your KiwiSaver periodically — especially when your goals change (first home, new job, growing family, approaching retirement) or if you haven’t looked at it in years.

Many New Zealand advisers can be paid by product providers, which may reduce or remove what you pay directly for KiwiSaver advice. However, this isn’t universal — some advisers charge fees, some receive provider payments, and some use a mix. It’s worth asking what you’ll pay, and how your adviser is paid.

Just as importantly, understand which providers (if any) your adviser has relationships with. Current disclosure requirements mean advisers must explain relevant fees, commissions, and conflicts of interest upfront.