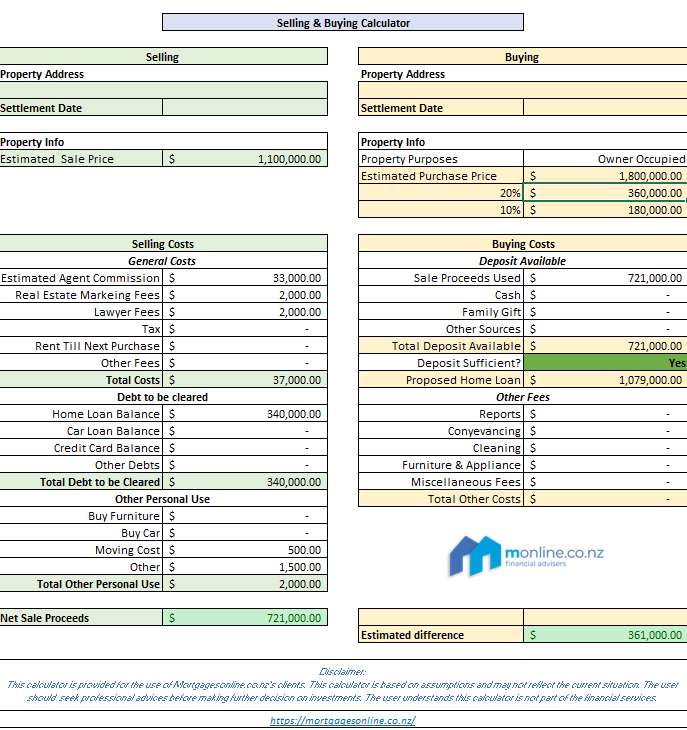

Getting into a bigger home or a better school zone is an exciting adventure. There are three main approaches to this really assuming you sell the old place. Some people don’t and turn the old one into a rental.

- Bridging finance

- Sell and then buy

- Buy and then sell

Each approach has its pro’s and cons and if you are able to get bridging finance things get a lot more simple. However there is a risk.

Bridging finance

This is where you(meaning we) try and obtain funding from a bank that will let you buy the new place and give you time to sell the old one. Say six months to a year. The beauty here is that you can make sure you have the right home in your hands before committing to sell. The moving becomes a lot easier, as in you have time do it in stages and then time to tidy up the old home before the sale.

The costs are higher as you do pay for two mortgages(if you have one currently and plan to get a bigger one). Also there is a risk that if the housing market isn’t in a good place later, you might find the sell price can leave you with more debt than you wanted. Or worse more debt than the bank is happy with. If you are unable to clear the bridging portion of finance by the deadline, both houses could be sold.

This risk can be mitigated by using the worst case scenario on the sale price when obtaining the funding.

Alternative approaches

Selling with a late settlement date, can give you time to quickly find a place. The risk here that you might need to Air BNB and find storage if you can not find something in time. Buying with a late settlement date and trying to quickly sell has a more severe risk in that you might find unable to settle if you can not sell for the right price, yikes. Legal advice might make you shudder at the costs that can be incurred if you are not able to settle on a purchase.

You could also buy on the condition of selling – meaning that if you can not sell you will be able to back out of the deal. You could sell in the same fashion – subject to buying a home. Both these options limit the pool of buyers and sellers you can approach which might make your price negotiation position weak.

What you should do right now

Talking to a good mortgage adviser like us is one thing. Of course we would say that but there is another vital piece of work you can start early. Get to know the market – start looking at the sale prices for the type house you will sell and buy. Take note of actual sale prices and the date when they sold. Not what is for sale but what has already sold. Many auction results are online and give up to the minute data.